Africa-Press – Rwanda. BK Capital has initiated coverage of MTN Rwandacell Plc with a price target of Rwf250, from the current Rwf170 per share at which its stock is trading at on the Rwanda Stock Exchange (RSE), while affirming its Buy rating on the stock.

This means that BK Capital analysts believe the stock price of MTN Rwanda is likely to increase in the future to reach Rwf250, a 48 per cent potential upside. With a Buy Rating, therefore, they recommend investors to buy MTN shares.

This comes on the back of increased cost pressures from both cost of sales and finance costs which led to a 28.9 per cent decline in MTN’s net profit to Rwf11.5 billion in 2023, despite the company registering an increase in revenue by 11.2 per cent to Rwf246.5 billion.

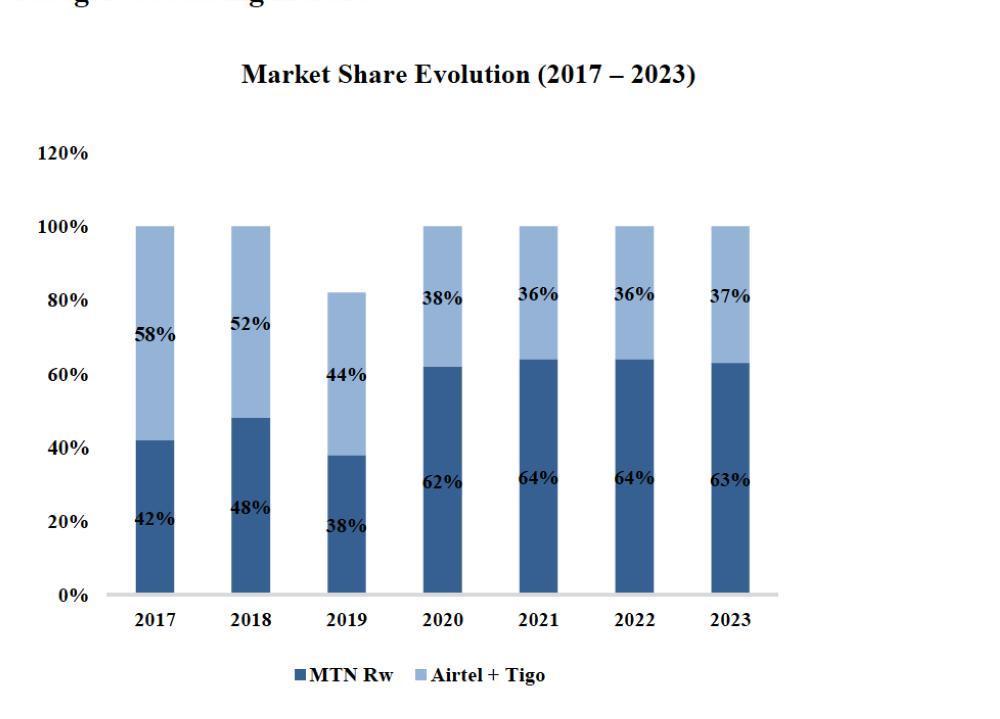

MTN Rwanda has consistently increased its market share since 2017.

The firm’s analysis suggests that despite the slow growth in 2023, MTN Rwanda is expected to perform better in the medium-term boosted by solid demand in its key products such as data and mobile money services.

ALSO Read: MTN Rwanda explains drop in earnings, projects better growth

Analysts are bullish that MTN’s strong brand and infrastructure, as well as demand for its data connectivity and mobile financial services will reduce their operating costs which would increase profits, and consequently increase cash flow.

“We analysed MTN as being uniquely positioned to leverage its strong market position to continue growing its subscriber base mainly for data due to an increase in smartphone penetration boosted by initiatives such as Macye Macye,” Lyna Muganwa, Investment Research Analyst at BK Capital told The New Times.

Muganwa also indicated that MTN is positioned to leverage its infrastructure and market position to address the growing demand for mobile financial services in Rwanda.

Cash flow to improve

BK analysts suggest that they expect MTN’s earnings before interest, taxes, depreciation, and amortization (EBITDA), a key metric for core operations, to grow faster than their investments in new equipment otherwise known as Capital Expenditures (CapEx), leading to more available cash.

Last year, EBITDA improved by 6.8 per cent to Rwf115.6 billion. However, the EBITDA margin – percentage that shows how much of a firm’s revenue is left as profit after core expenses – dipped by 1.9 percentage points to 46.4 per cent.

The company attributed the negative growth in EBITDA margin to the new mobile interconnection rules introduced by the Rwanda Utility and Regulatory Authority (RURA).

Muganwa said despite the negative EBITDA margin growth seen last year, MTN’s ability to manage its topline gives them a positive view of the trajectory of EBITDA growth in the future.

Meanwhile, analysts expect average revenue per user (ARPU) to rise, suggesting that MTN will earn more revenue from each customer it services, potentially due to increased internet usage, mobile financial services, or higher service fees.

If MTN spent a smaller portion of its sales revenue on capital expenditures over time, BK Capital said, this could free up more cash flow.

Another key attribute that analysts give investors is the expectation that MTN will see its debt levels reducing, and if the company pays down debt, they will eventually have less interest to pay, which will again improve their cash flow situation.

That will, in turn, improve earnings per share and dividends to shareholders, analysts said. They suggest a 50 per cent payout ratio – the percentage of profits distributed as dividends – will be returned to shareholders by 2028.

MTN stock undervalued

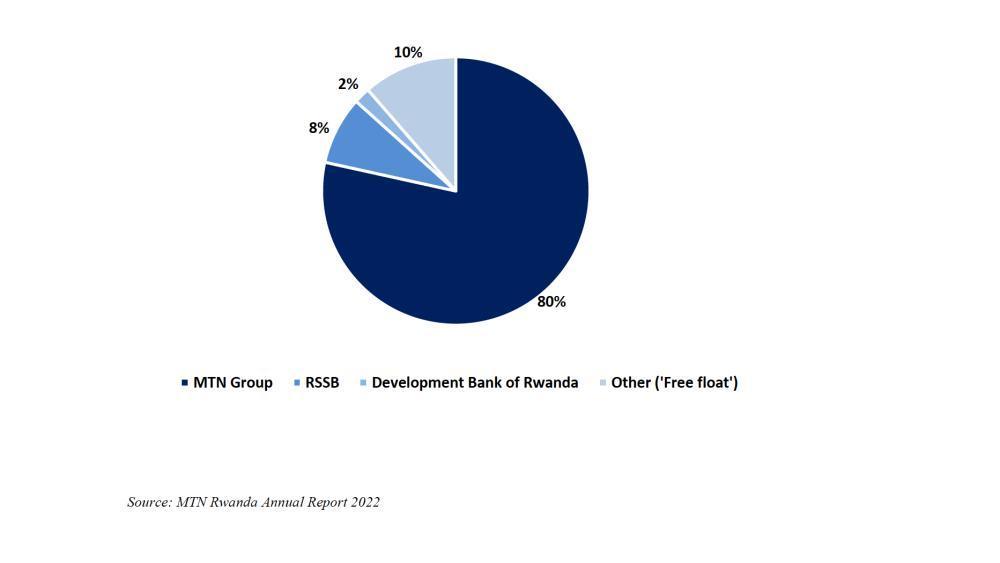

MTN Rwanda currently controls the telecommunications market with a 62 per cent market share. The firm listed 20 per cent of its shareholding at an initial listing price of Rwf269 per ordinary share on the RSE in May 2021.

MTN’s stock was trading at Rwf170 at the time of initiation coverage, which analysts believe is currently undervalued compared to similar companies in the region.

MTN Rwanda Shareholding Structure and Free Float.

They said the company’s current valuation is 3.5 times its EBITDA, suggesting that MTN’s valuation is 40 per cent lower than the average valuation of similar companies in Sub-Saharan Africa.

“We are sending signals to investors that look, this is an undervalued stock compared to the peers in the region. You should pay close attention to it,” Muganwa noted.

MTN has consistently gained market share, growing its subscriber market base from 42 per cent in 2017 to 62 per cent as of December 2023, supported by its market position, network coverage advantages and brand equity.

Analysts estimate MTN’s revenue market share to be at 85 per cent, up from 67 per cent in 2017, including 81 per cent and 99 per cent data and mobile money revenue shares, respectively.

With such a large share of the market, MTN can potentially spread fixed costs such as capital expenditure and operating expenses over a much larger customer base, which can lead to higher profit margins over their rival, Airtel Rwanda with a smaller market share.

Other key metrics

MTN Rwanda’s 11.2 per cent (Rwf246.5 billion) service revenue performance in 2023 came on the back of growth registered in data, financial technology, and its enterprise business segments.

Total subscribers increased by 6.5 per cent year-on-year to 7.3 million. The increase did not translate into increased voice revenue. MTN’s voice revenue declined by 21.3 per cent to Rwf84 billion in 2023.

Voice currently accounts for 34 per cent of MTN’s service revenue.

According to analysts, voice revenue will remain under pressure for the foreseeable future with voice average revenue per user (ARPU) receiving hit from competitive behavior as well as from falling termination rates.

At the same time, over-the-top technology services such as WhatsApp, Facebook, and Instagram will increasingly move ‘voice traffic’ onto other platforms as data penetration rises in tandem with improvements in network quality and with higher smartphone adoption.

“The recent change in regulation that now enables MTN to roll out its own 4G network (on top of existing infrastructure) shall prove to be positive for ARPU and enhance return on historical CapEx investments,” BK Capital noted.

MTN grew its active data customer base by 14.3 per cent to 2.6 million in 2023. This translated into data revenue growth of 11.2 per cent to Rwf45 billion year-on-year.

BK sees this growing further. They predict MTN’s data subscribers will grow at 7 per cent compound annual growth rate through 2028, with revenue growing at 14 per cent compound annual growth rate in the same period.

Mobile data currently accounts for 18 per cent of service revenue and analysts forecast this shall grow to a 23 per cent contribution by 2028, driven by a combination of higher average revenue per user and increasing connectivity.

Active data users are expected to eventually reach 45 per cent of total subscribers and data revenue to reach Rwf88 billion over the same time frame.

This positive growth forecast, however, might be threatened by changes in the competitive landscape such as if Airtel Rwanda aggressively introduces competitive products, and this could lead to profit margin erosion.

There are also regulatory risks aimed at increasing affordability or encouraging new entrants such as the introduction of new interconnection rules by RURA which capped interconnection rules at zero for a period of one year.

Muganwa said that, how MTN allocates its capital, could be a downside to their forecast, insisting that it is, for instance, too early for the telco to invest heavily into 5G network rather they should inject more into accelerating 4G accessibility and affordability.

For More News And Analysis About Rwanda Follow Africa-Press