Africa-Press – South-Africa. South Africa has been stuck in a vicious cycle where weak economic growth translated into declining tax revenue and falling creditworthiness, increasing borrowing costs and depressing growth.

The state has been trying to break out of this cycle since 2013, with various attempts at kick-starting the economy through increased state spending failing.

Instead of boosting economic growth, increased state spending led to persistent budget deficits, resulting in a substantial debt burden.

Symmetry chief investment strategist Izak Odendaal explained that South Africa defied economic convention in entering this vicious cycle.

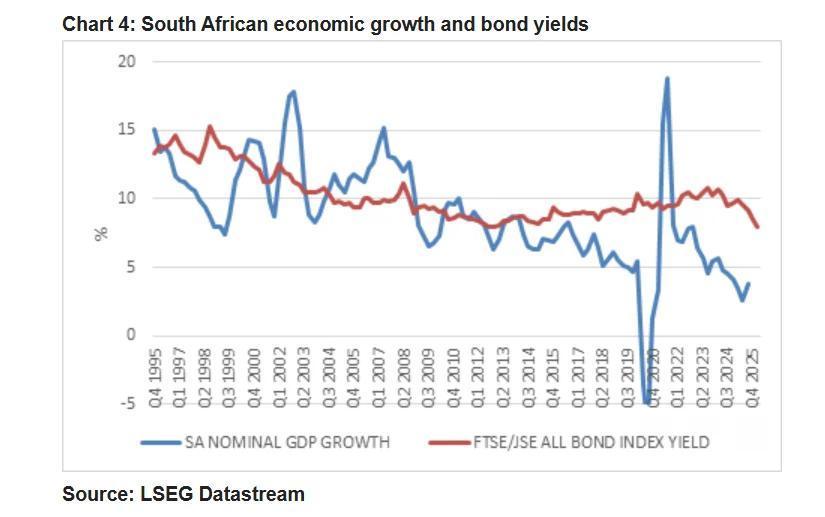

“It is an old rule of thumb that bond yields should move in line with nominal GDP growth, which is real growth with inflation,” Odendaal explained.

This means that South Africa’s bond yields have typically hovered above 7% at the front end of the curve and above 10% on longer-term debt.

As a result, South Africa paid a relatively high premium to service its debt. Coupled with a growing debt pile, the country is now paying over R1 billion a day in interest payments.

This is effectively “dead money” that could be better used to invest in healthcare, education, and economic growth, rather than to pay off past expenditure.

Odendaal explained that South Africa began breaking economic convention in 2013, when the country’s growing debt pile began impacting its sovereign credit rating.

“Bond yields should move in line with nominal GDP growth. This was the case in South Africa too, until around 2013, when the economic performance deteriorated sharply, and with it, the government’s creditworthiness,” Odendaal said.

“The latter put upward pressure on bond yields, kicking off a vicious cycle since weaker growth meant lower tax revenues, further losses in creditworthiness, and higher borrowing, which further depressed growth.”

This cycle has played out over the past decade, with South Africa’s economic growth hovering at 1% per annum and debt-servicing costs surging.

The relationship between bond yields and nominal GDP growth can be seen in the graph below, courtesy of Odendaal.

Breaking the cycle

South Africa has been trying to break out of this cycle for the past five years, and Odendaal said the data points to it successfully ending the decade of despair.

The National Treasury has been implementing fiscal consolidation in earnest since the appointment of Enoch Godongwana as Finance Minister in 2021.

Godongwana is in the second year of his second term as Finance Minister and has overseen the slow and painful process of fiscal consolidation.

This process is beginning to bear fruit after years of containing government spending and squeezing more tax revenue from a stagnant economy.

The painful process is necessary after 15 years of mismanagement, which resulted in skyrocketing government spending, with very little to show for it.

South Africa’s economy stagnated, averaging an annual growth rate of 0.8% for the past decade, pushing government debt as a share of GDP to over 77%.

Government debt as a share of GDP has more than tripled since Trevor Manuel left office in 2009, when it was a mere 26% of GDP and declining.

Odendaal explained that fiscal consolidation has resulted in South Africa being closer than ever to achieving a full budget surplus.

In his most recent Medium-Term Budget Policy Statement, Godongwana outlined the rewards of fiscal consolidation, which is the culmination of years of efforts.

Odendaal said this is not a turning point in fiscal policy, but a turning point in investor perception of South Africa as a country with runaway debt.

South Africa is set to record a wider primary budget surplus of 0.9% of GDP in the current financial year, with this widening to over 2% in the next three years.

This means the government is bringing in more revenue than it is spending, excluding debt-servicing costs. It is on track to do this for three years in a row.

A primary budget surplus will result in the government’s debt pile stabilising at 77.9% of GDP in the current year before gradually beginning to decline. In effect, it halts growth in the debt pile.

With faster economic growth forecasted, the picture should improve further as Godongwana’s department remains dedicated to driving reform through Operation Vulindlela.

“We are in the early stages of closing the gap and reversing the vicious cycle. But to do so requires the Budget to stick to fiscal discipline while accelerating growth-enhancing reforms,” Odendaal said.

For More News And Analysis About South-Africa Follow Africa-Press